What sounded like a futuristic movie a few years ago is becoming more and more reality: connected, highly-automated and autonomous vehicles sharing the roads. With the horizon of having at least semi-automated vehicles being commercially launched in the next few years, insurers need to prepare themselves to radically change traditional risk scoring and segmentation of their customer portfolio: from driver-centric to vehicle-centric.

In April 2019, Tesla’s founder Elon Musk first talked about launching insurance for the brand’s electric vehicles. However, upon roll-out some months later, the insurance product failed – simply because the tariffs were contradictory to what Musk promised higher than existing ones with other insurance companies. Last year – take two: Musk came up with a personalized priced insurance based on driving behavior. “Ultimately, where we want to get to with Tesla Insurance is to be able to use the data that’s captured in the car, in the driving profile of the person in the car, to be able to assess correlations and probabilities of a crash and be able then to assess a premium on a monthly basis for that customer.”

Is the case of Tesla, in which an OEM becomes an insurer using data directly collected from the vehicle, becoming mainstream? Will the traditional insurance models become obsolete? Only if traditional insurers are not prepared for the actual digital challenge in automotive: getting their hands on car data and paving the way for Connected and Automated Vehicles’ (CAV) insurance.

During the last two decades, vehicular technologies have been advancing considerably. From the integration of vehicles with global navigation satellite systems to the development of more sophisticated driving assistance features such as adaptive cruise control and lane-keep assist, the vehicular industry has experienced many improvements leading to a more efficient and secure driving experience.

With the idea of making the driving tasks more and more automated, vehicle manufacturers have been integrating technologies using communication and surveying systems like radar, LiDAR, and cameras. As a consequence, the way drivers interact with their vehicles is drastically changing, with well-defined levels of automation, from level 0 (no automation) to level 5 (full automation).

There is great enthusiasm about the benefits of CAV in society, mainly in road safety. According to reports from the EU and the US, human error is the leading cause of more than 90% of accidents. Thus, it is expected that removing this component from the equation will impact significantly the number of accidents that happen on the roads. However, this change will not happen overnight, and CAVs will coexist with human-driven vehicles for many years. This implies that even though CAVs prove to drive safely, they will need to respond efficiently to human-driven vehicles’ errors. Yet, the risk induced from these non-automated vehicles is expected to shrink as the penetration rate of CAVs increases over time.

The severity of accidents is another component that needs close evaluation. In situations where CAVs cannot successfully avoid a crash, they typically take mitigation strategies to reduce the gravity of the impact. Therefore, one might expect that CAVs will contribute to a reduction in road severities. However, from an insurance perspective, the cost of accidents remains to be studied since the technology inside these vehicles is more costly to repair or replace than conventional ones. For instance, consider an accident that damages the vehicle’s sensors; apart from the traditional mechanical repair cost, it introduces costs associated with replacing the sensors and the inherently qualified workmanship to make them fully functional.

The traditional motor insurance sector has been focusing on driver-centric analyses to build pricing models that reflect a fair segmentation of their drivers’ portfolio. This segmentation is closely related to the drivers’ risk profiles and constitutes the basis of the tariff insurers charge to their customers (i.e., insurance premium).

Motor insurers have focused on drivers’ demographics, claims history, and vehicle information to achieve segmentation by building statistical models covering traditional driving risks. Examples of these include the vehicle’s brand and model, driver’s age, place of residence and years licensed, or the number of claims. However, these models have the disadvantage of being static, i.e., they are computed on product launch. Moreover, as they depend on the driving history, it is challenging to segment drivers with little driving experience into safe and risky groups.

Usage-based Insurance (UBI) frameworks incorporate dynamic driving variables such as driving behavior and context to understand better the risk involved in the policyholder’s portfolio. To illustrate the concept, consider two newly-licensed drivers with similar demographic characteristics. In a traditional-and-static insurance scheme, they would be classified in the same group. By incorporating dynamic variables like the usual road types, driving time in congested areas, and obedience to traffic rules, insurers can gain an advanced level of understanding about their risk differences. In other words, dynamic variables related to driving behavior and context have enabled insurers to enhance their insurance models’ predictive power, improving pricing schemes and thus increasing the competitiveness of the offer.

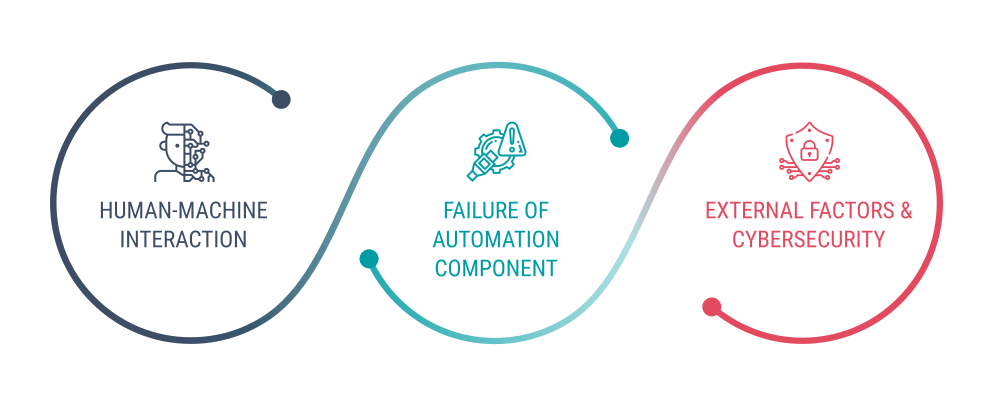

With the integration of CAVs, traditional insurers’ predictive power is being challenged due to the emerging risk factors. Appropriate risk assessment models will need to evaluate not only driving dynamics, but also the human-machine interaction, the failure likelihood of automation components, and potential threats from external factors such as cybersecurity and surrounding vehicles’ risk. Also, the safety benefits introduced by ADAS features indicate a potential reduction in exposure to accidents. However, these benefits might be impaired by adverse driving contexts like heavy rain and incorrect uses of automated systems.

At the intermediate automation levels, the automated system’s usage and performance will take more and more relevance in the risk scoring. When the autonomous system fails at handling a particular situation, a common indicator is reflected by what is known as a system-initiated disengagement event. In these scenarios, the vehicle sends several warning signals to the driver to take over the driving task, and the driver’s reaction to them becomes a proxy to risk. Should the driver be distracted and fail to respond to these indicators, the system needs to take an emergency maneuver to avoid hazardous consequences. On the other hand, a driver-initiated disengagement event generally indicates a lack of trust in the system, and therefore the benefits of automated features are diminished.

As the automation level increases, insurance products’ focus will need to shift from driver-centric to vehicle-centric models to reflect the level of risk and offer competitive premiums accurately. The expected reduction in accident frequency indicates that the motor insurance market size will shrink over time. Thus, data-driven approaches that efficiently capture the new vehicular technologies’ risks will be essential for a successful adaptation to the upcoming vehicular transition.

There are undergoing investigations to perform risk scoring for CAV in different automation levels. Determining what “safe” means in terms of the automated vehicle is not straightforward. Automated vehicles would have to be driven hundreds of millions of miles to give statistical evidence about their safety in terms of traffic injuries and fatalities. Moreover, the quality of automation systems will likely vary significantly between different brands, models, and AI software versions, requiring continuous monitoring of CAV data. The mass of required driven distance is an impossible proposition if the objective is to provide evidence about their safety performance before their general deployment on public roads. The development of CAV would need innovative methods to demonstrate safety.

A potential approach involves a mixture of real-world driving scenarios and simulations around safety-relevant events. For instance, Waymo analyses the situations that require the driver to take over the driving task using a counterfactual (i.e., what if) scenario, focusing on how the vehicle would have reacted if it had continued in automated driving mode. The relevant fact about this type of perspective is that the simulations are more realistic than synthetically-simulated scenarios.

Public data usage arises as a significant factor in promoting transparency and objectivity for risk analyses in a CAV ecosystem. The California DMV initiative to promote AV safety-relevant incidents reports is a relevant approach towards this end. However, AV accident reports are not yet statistically significant to weight risk objectively. There is also a need to have similar reporting campaigns in other parts of the globe, hopefully in a standardized way.

Naturalistic data collection initiatives with semi-automated vehicles are encouraged to investigate the transition towards CAV in data-driven risk assessment. It is worth noting that the data collection campaigns should avoid irrelevant driving data to reduce technical constraints, and therefore to separate the suggested reporting rate into continuous, time-window, and discrete.

As for higher automation levels, CAV time-series data coming from LiDARs, radars, or vision systems could be added. Such an extended feature set might enable holistic analyses of the triad composed of the driver, the vehicle, and their interaction. The importance of each component might vary according to the level of automation.

The availability of this information might help insurers understand their policyholders’ exposure by analyzing how and where they interact with automated features and the automated system’s performance. As the penetration rate of CAV increases, the link between these variables to severity and loss information would help them provide fair premiums for the whole portfolio, regardless of the automation level. This might enable sustainable development, transparency, trust, and regulation in the insurance market and eventually determine the insurer’s successful adaptation to the transitioning vehicular ecosystem.

Key takeaway: Automation technology is an enabler for making the roads safer. As of the deployment of the first CAVs, the transfer of risk from driver-oriented to vehicle-oriented situations is inevitable. To avoid traditional insurance obsolescence, change becomes mandatory: it’s now time to invest in adequate models to assess CAV risk, starting from the lower levels of automation and preparing the field for the fully automated scenario.

| Cookie | Duration | Description |

|---|---|---|

| cookielawinfo-checkbox-analytics | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics". |

| cookielawinfo-checkbox-functional | 11 months | The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional". |

| cookielawinfo-checkbox-necessary | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary". |

| cookielawinfo-checkbox-others | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other. |

| cookielawinfo-checkbox-performance | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance". |

| viewed_cookie_policy | 11 months | The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data. |

Test drive our API Suite for 30 days!

Tell us a bit about yourself, and we’ll get in touch with you in no time.